Financial Accounting

01 Financial Statements

学习目标

- Explain why accounting is the language of business.

- Explain and apply underlying accounting concepts, assumptions and principles.

- Apply the accounting equation to business organizations.

- Evaluate business operations through the financial statements.

- Construct financial statements and analyze the relationships among them

- Evaluate business decisions ethically .

学习资源

ifrs.org

iasplus.com

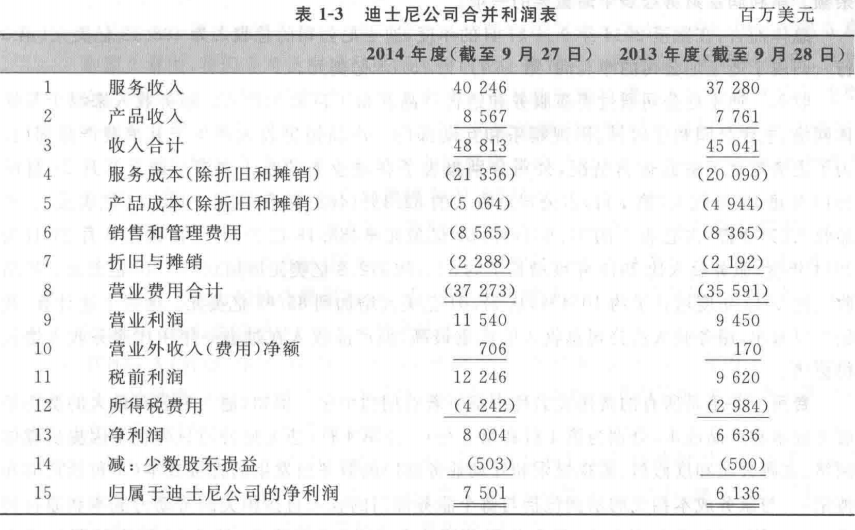

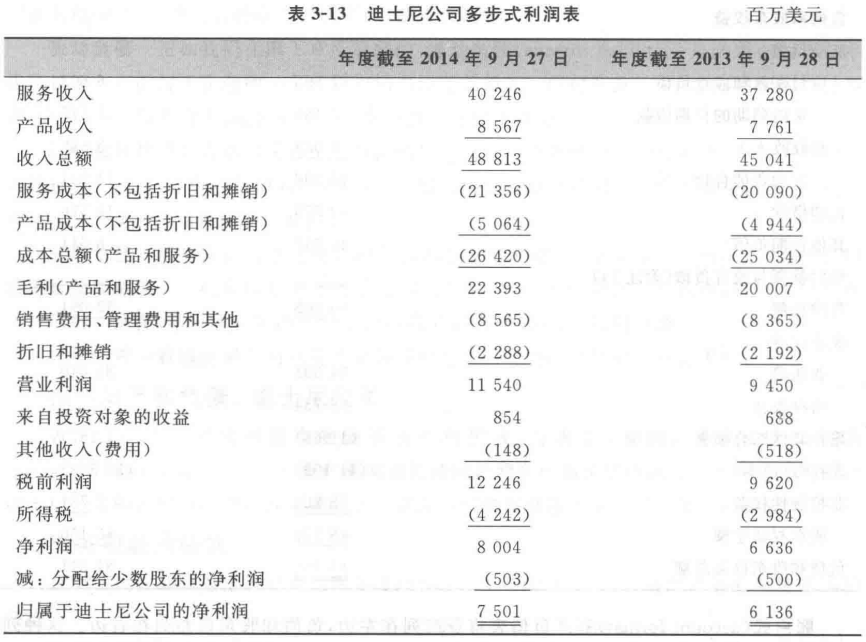

迪士尼的例子

合并利润表

why accounting is the language of business

measure , process data into reports , communicates results to decision makers.

who use accounting

two kind of accounting

- financial accounting . outside to : investors , creditors , government agencies , public

- managerial accounting. inside . budgets , forecasts , projections.

the various forms of business organization and the different

Proprietorship 个体户,Partnership 合伙制,LLC 有限公司,Corporation 股份公司

owners and 'personal liability of owners for business debts' is different

corporation double taxation : corporation pays income tax , stockholders taxed on dividends(股息红利).

china have 3 accounting system

- one for public

- one for smalll & medium

- one for

Underlying accounting concepts and assumptions , principles.

两种国际专业标准

GAAP : 美国的 Formulated by the financial accounting standards board (FASB)

IFRS : International Financial Reporting Standards

Accounting Assumptions & Principles

Relevance , Faithful .

Entity Assumption , Continuity Assumption, Historical Cost principle , Stable Monetary unit assumption

资产应该在他们购买的日期以真实成本被记录。货币的购买力应稳定。

Accounting equation

Assets = Liabilities + owner's equity (stockerholder's equity)

会计名词

revenues , expenses, dividends 股利,

net income , net earning 净盈余, net profit 净利润,net loss 净亏损。

Assets

- cash , cash equivalents

- Inventories

- Account receivable

- Property , Plant , equipment

Liabilities

- Accounts payable

- income taxes payable

- long-term debt

Owner's Equity

corporation's equity is called stockholders' equity and it has two parts:

- Paid-in capital 实收资本 (common stock)

- Retained earning 留在收益

- dividends: distribution of the company's earning to its shareholders.

'Revenues for the period' - 'Expense for the period' = 'Net Income'(净收益 )

'beginning balance of the retained Earning' +/- 'Net Income' - 'Dividends for the period' = 'Ending balance of Retained earnings'

Dividends (股息,红利):distribution of assets to the stockholders.

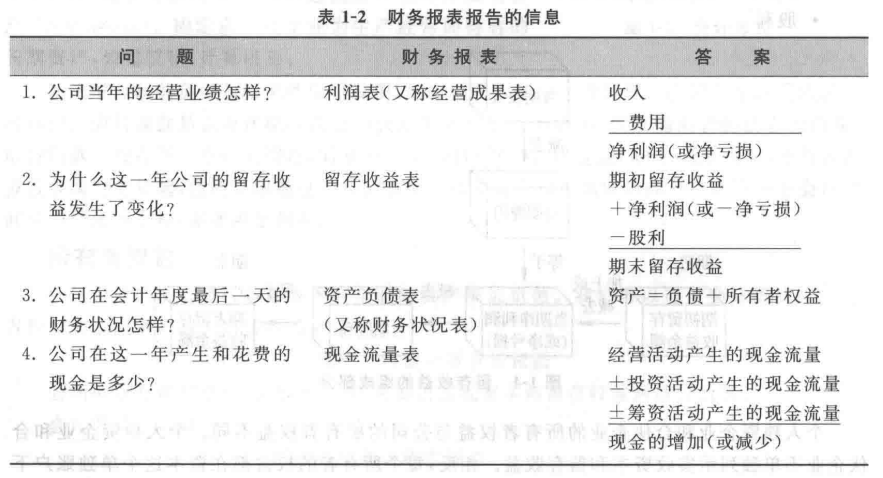

Evaluate the business operations through the financial statements.

income statement, Retained Earning , Balance Sheet , Cash Flows . 销售表,收益表,财务平衡表,现金流量表。

合并利润表

留存收益表

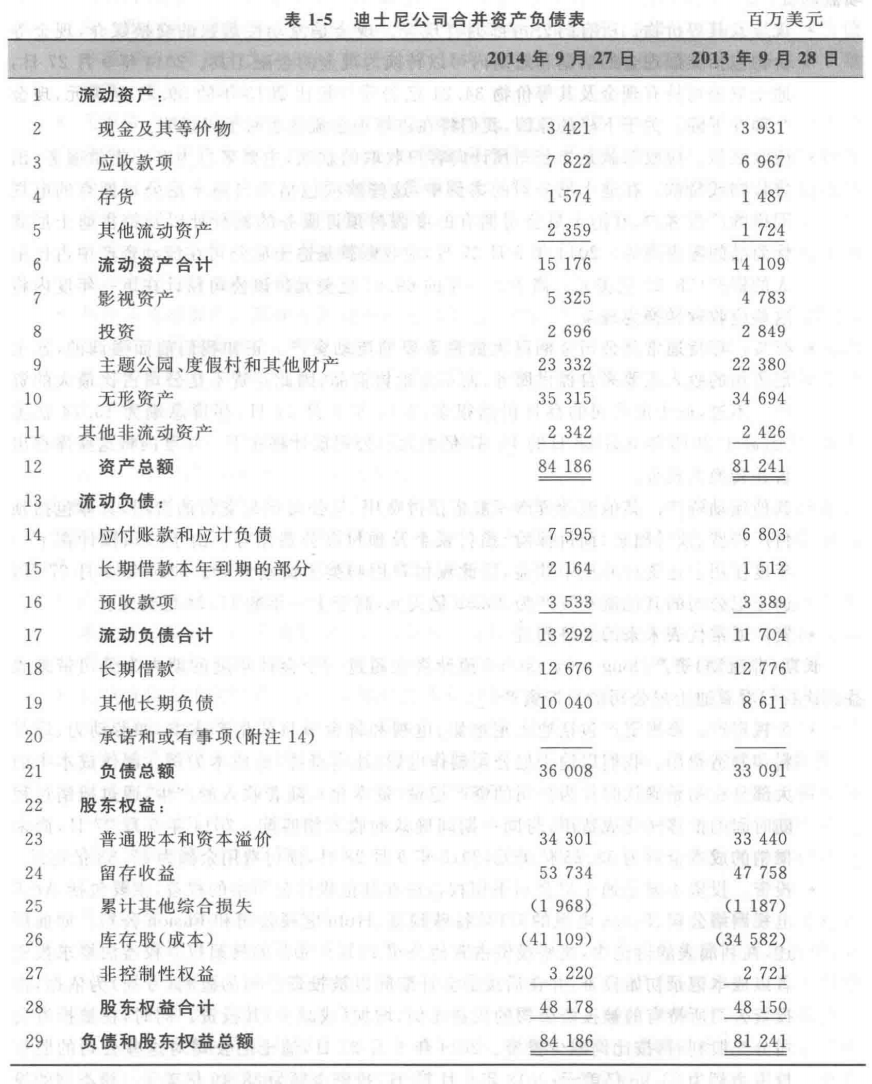

资产负债表

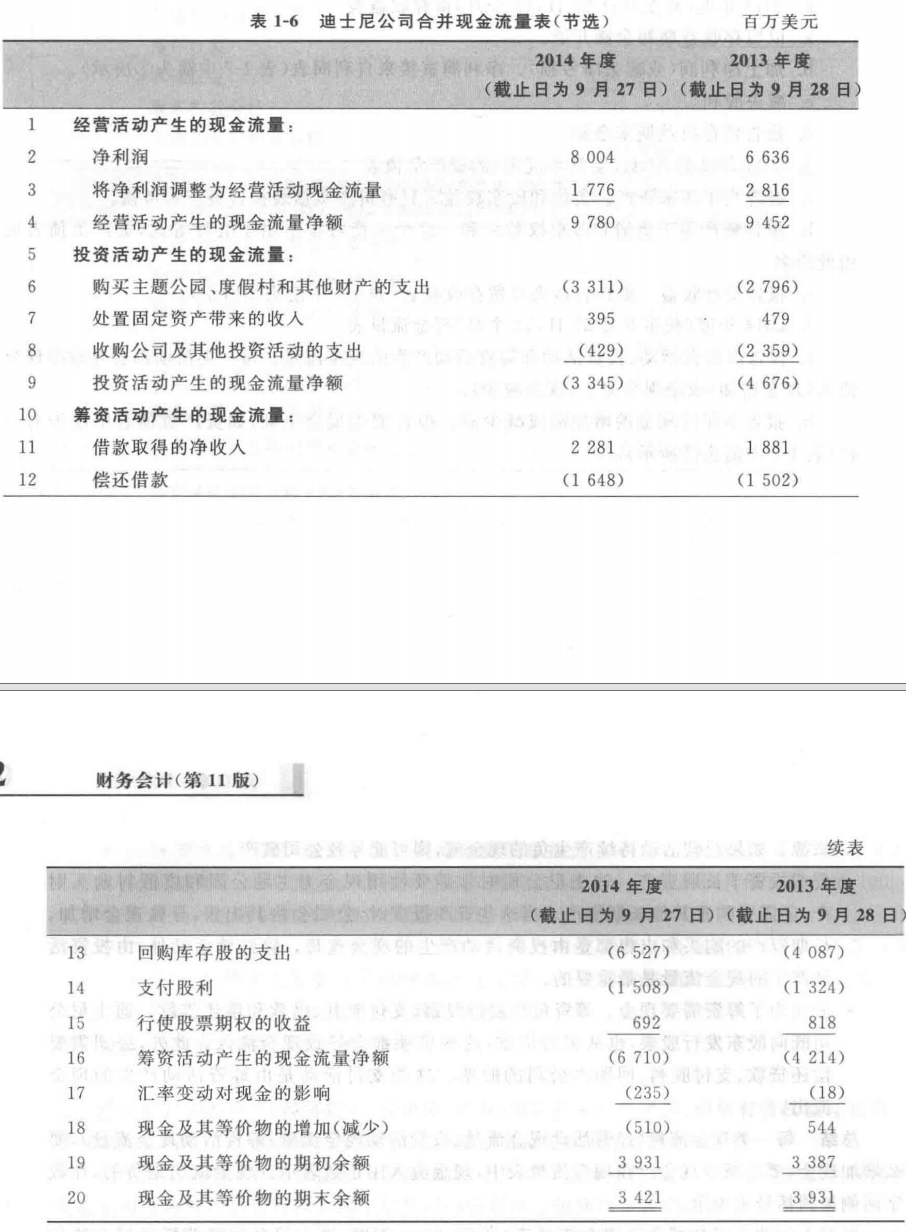

现金流量表

经营活动,投资活动,筹资活动。

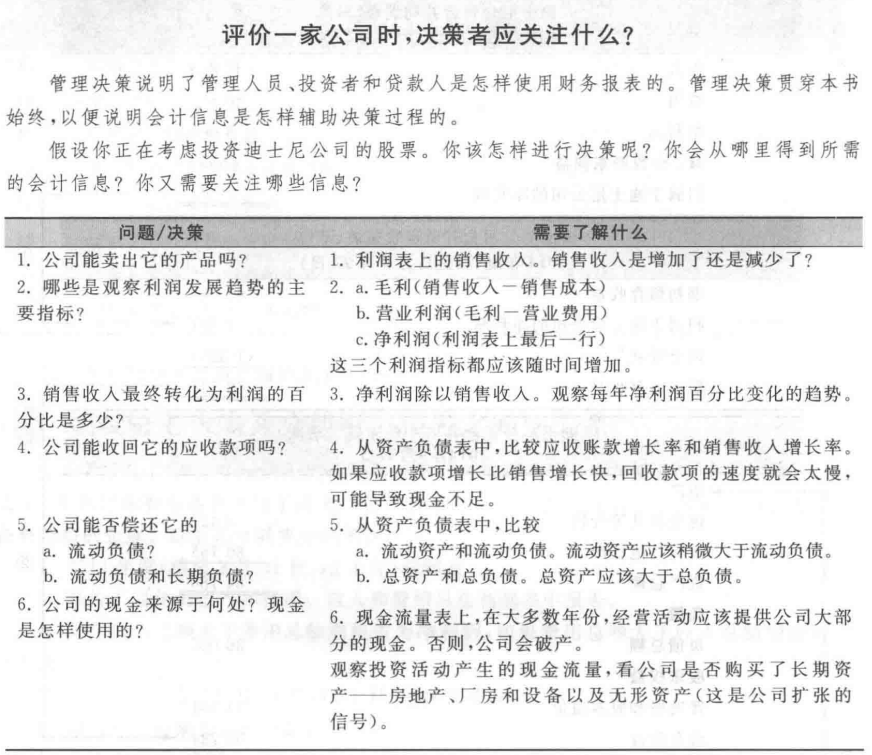

评价一个公司,决策者关注什么

Cash Flow

- operating activities

- invest activities

- financing ... (pay or borrowing)

Relations among the financial statements

各报表之间的关系。

Evaluate business decision ethically

Economics , Legal , Ethical .

02 Transaction analysis

learning objectives

- what is a transaction

- define accounting and list and differentiate between different types of accounts

- show the impact of businesses transactions on the accounting equation

- analyze the impact of business transaction on accounts

- record transaction in the book

- Construct and use a trial balance

1. what is a transaction

a transaction is any event has a financial impact on the business and can be measured reliably .

每一项交易包括两个方面:付出了什么,相应地收到了什么。

会计循环: 确认交易, 分析其对会计等式的影响 , 在日记账中记录交易, 将其过到分类账中。

2. define accounting and list and differentiate between different types of accounts

the accounting equation express the basic relationship of accounting

an account is the record of all the changes in a particular asset , liability , stockholders' equity during a period .

Assets:cash ,revenue , accounts receivable , Inventory , 预付费用,investments , property, Plant, Equipment.

Liabilities :accounts payable , notes payable , accrued liabilities( liabilitity for an expense you have not paid ) .

Stockholders' Equity: Common stock , Retained Earning( cumulative net income minus net loss and dividends over the company's life) , Dividends, Revenues , Expense .

3. show the impact of business transactions on the accounting equation

4. analyze the impact of business transaction on accounts

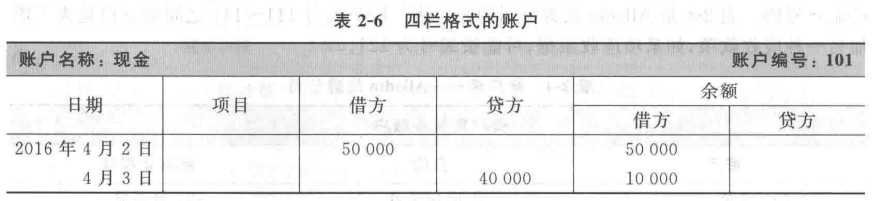

T-Account , left : debit ; right : credit .

经济交易的会计处理。所有的经济交易都包括:付出什么,得到什么。因此会计是基于复式记录体系而建立的,它记录交易对经济主体的双重影响。double entry system , records dual effects of each transaction.

the T - Account

资产的增加记在左边,减少记在右边。

负债和所有者权益增加记在右边,减少左边。

5. record transaction in the books (日记账和分类账)

journal & ledger

日记账到分类账称为 过账。

6. construct and use trial Balance

lists all accounts with their balances.

账户表(chart of accounts)

03 Accrual Accounting & Income

1 explain how accural accounting differs from cash-basis accounting

权责发生制和收入计量,会计期间 time-period concept

权责发生制可以避免一些在计付现结下的道德问题。

2 apply the revenue and expense recognition

when to record revenud , what amount.

expense recognition principle. expense and revenue.

3 adjust the accounts

Deferrals , Depreciation , Accruals (the opposite of a deferral)

prepaid expense are assets .

accumulated depreciation ---> Depreciation expense

unearned service revenue . 没有收入的费用发生时确认。

4 construct the financial statements

基于流动性对资产进行分类

账务报表的格式

资产负责表格式: 报告式,账户式

利润表格式: 单步式,多步式。

5 close the books (结账)

Prepares the accounts for the next period. close temporary accounts. 永久性账户(不做结账处理,金额延续)

closing entries 结账分录合收入类账户和费用类账户的余额归零。这与在比赛结束后记分牌归零是同样的道理。

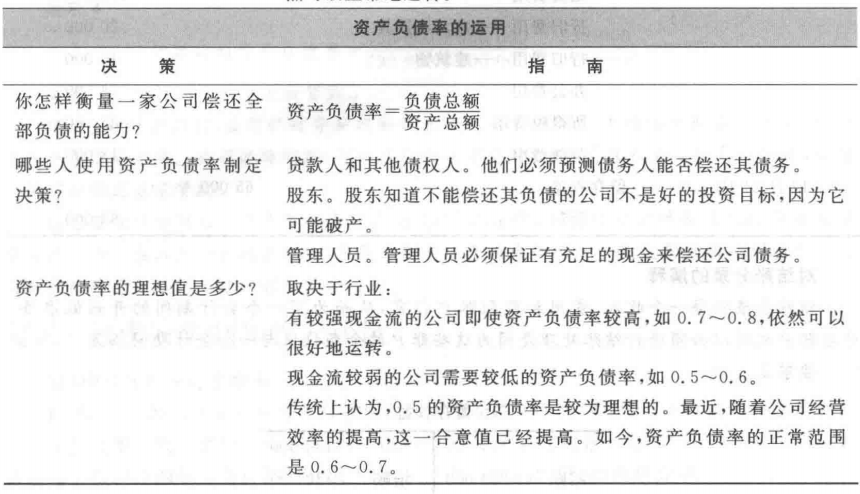

6 analyze the evaluate a compan's debt paying ability

current ratio(流动比率) : current assets / current liabilites 1.2~1.5 is good

Debt ratio: total liabilities / total assets

使用营运资本净额,资产负债率,流动比率,评价债务偿付能力。

流动比率

- 流动比率大于1通常被认为是良好的,这意味着公司有足够的流动资产来覆盖其流动负债。

- 流动比率低于1可能表示公司面临短期偿债压力,但也要结合行业标准和其他财务指标一起分析。

- 流动比率过高可能意味着公司持有过多的现金或流动资产,这可能不是最有效的资本使用方式。

费用

05 短期投资与 receivable

cash flow are solely payment of principal and interest . 本金&利息。

Amortised cost 均摊成本

FVTPL fair value throuth profit loss

FVOCI Fair value through other comprehension income

06 Inventory & cost of good sold

Depreciation

3种折旧方法: 直线,单元,加速折旧。

Depletion 耗尽

为什么无形资产要摊销? 有时间周期。

Cost vs Expense

成本和特定资产相关。

Finance Equity method < 20%

subsidary > 50%

invesment in associate

08 long term investments & time-valued of money

10 StockerHolders's Equity

the feature of a corporation

stockerholder's rights

class of stock

- common stock

- preferred stock

par-value vs no-Par value

account for the issuance of stock

treasury 回购股票

compension stock 补偿股票

account for retain earning

dividends and splits

- declaration date

- date of record

- payment date

Liabilities

收入准则

金融准则

保险准则

租赁准则

新型业务的兴起,商业模式的变化 。

判定融资租赁

- 金额

- 租期占寿命大于 75%

- 专有使用(转让成本极高)

- 产权转让极低成本,也可行。

经营租赁,融资租赁。

- 已识别资产

- 谁用

- 如何用

- 合同包含租赁 , 合同不包含租赁。